On This Page: [hide]

The web hosting industry has evolved far beyond simple file storage on rented servers. What started as a straightforward infrastructure business now encompasses cloud computing, edge networks, managed services, and increasingly, artificial intelligence. The numbers reflect this transformation: depending on how you measure it, the global hosting market ranges from $125 billion to $195 billion in 2025, with projections suggesting it could triple or quadruple by decade’s end.

The big picture: Cloud infrastructure spending crossed $100 billion in a single quarter for the first time in Q3 2025. AWS, Microsoft Azure, and Google Cloud control over 60% of that market, but traditional hosting providers aren’t standing still. Private equity continues pouring billions into hosting consolidation plays, while sustainability concerns are reshaping how data centers operate. The industry is simultaneously growing and transforming at a pace that makes five-year forecasts feel like guesswork.

Data verified February 2026. Statistics sourced from Synergy Research Group, Fortune Business Insights, Grand View Research, and industry reports.

Market Size: The Numbers Depend on What You’re Counting

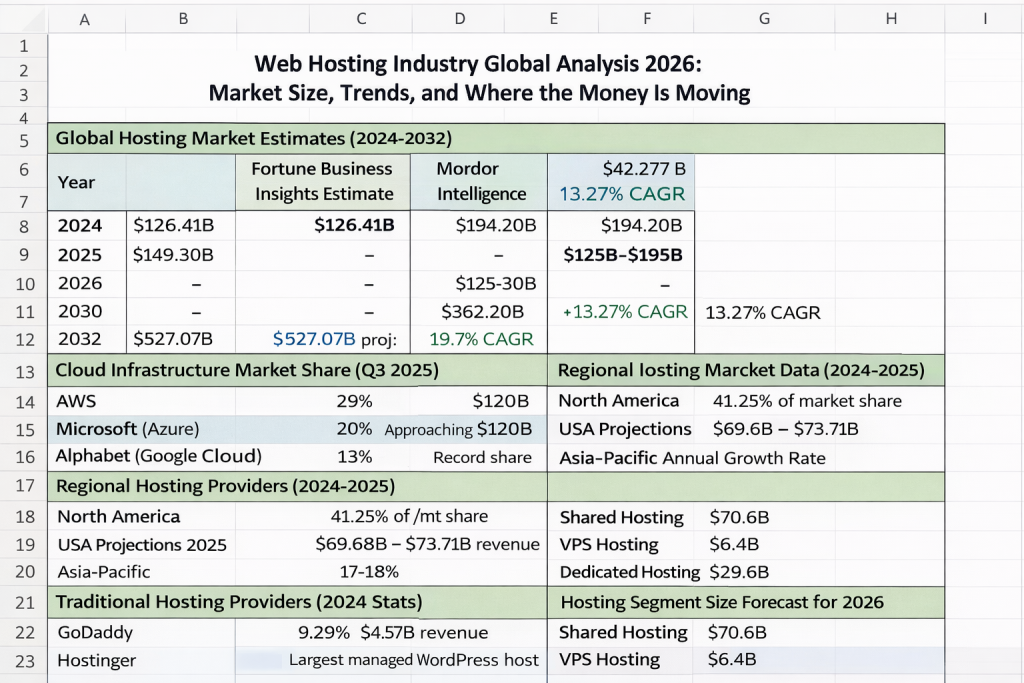

Ask five research firms for the global web hosting market size and you’ll get five different answers. This isn’t sloppiness. It reflects genuine disagreement about where web hosting ends and adjacent markets begin. Does cloud infrastructure count as hosting? What about CDN services, managed platforms, or domain registration bundled with hosting? The definitions matter.

Fortune Business Insights valued the global web hosting services market at $126.41 billion in 2024, projecting growth to $149.30 billion in 2025 and $527.07 billion by 2032. That trajectory implies a 19.7% compound annual growth rate, which would represent explosive expansion if realized. Mordor Intelligence offers a more conservative view, placing the 2025 market at $194.20 billion with growth to $362.20 billion by 2030 at a 13.27% CAGR.

The wide range reflects different methodologies. Some analysts count only traditional hosting services. Others include cloud infrastructure, platform-as-a-service offerings, and managed enterprise solutions. What’s consistent across estimates is the direction: this market is growing fast, driven by digital transformation that shows no signs of slowing.

Breaking down by geography, North America dominated in 2024 with 41.25% market share and $52.14 billion in revenue. The United States alone represents the largest single national market, with projections suggesting $69.68 billion to $73.71 billion in hosting revenue for 2025. Europe follows as the second-largest regional market, while Asia-Pacific claims the fastest growth rate at 17-18% annually.

The Hyperscaler Dominance: AWS, Azure, and Google Shape Everything

Any analysis of the hosting industry must start with the cloud giants. Amazon Web Services, Microsoft Azure, and Google Cloud Platform don’t just dominate cloud infrastructure. They’re reshaping expectations about what hosting means, forcing traditional providers to adapt or find defensible niches.

Global cloud infrastructure spending reached $106.9 billion in Q3 2025, marking a 28% year-over-year increase and crossing the $100 billion quarterly threshold for the first time. For the full year, cloud infrastructure revenues are projected to exceed $400 billion. These numbers dwarf traditional hosting markets, illustrating how thoroughly the industry’s center of gravity has shifted.

AWS maintains its position as market leader with 29% share as of Q3 2025, though that figure has declined steadily from approximately 33% in late 2021. The company still leads in absolute revenue, but its growth rate has slowed to roughly 17% year-over-year. AWS hosts more than 124 million websites worldwide, including major properties like Reddit, Netflix, and Zoom. Among the top 1 million websites, AWS powers nearly 26%.

Microsoft Azure stabilized at 20% market share with annualized revenue approaching $120 billion. Azure has consistently outpaced AWS in growth rate, and its enterprise integration through Microsoft 365 and Teams creates sticky relationships that competitors struggle to replicate. The company’s aggressive AI investments, especially its partnership with OpenAI, position it well for workloads that demand serious compute resources.

Google Cloud achieved 13% market share in 2025, representing record territory for the platform. Despite smaller absolute size, Google demonstrated the strongest growth momentum among the top three hyperscalers. The company’s data analytics and machine learning capabilities attract customers with specialized needs that commodity hosting can’t address.

Perhaps the most dramatic trend is AI-driven growth. GenAI-specific cloud services expanded 140-180% in Q2 2025, while GPU-as-a-Service revenues grew more than 200% year-over-year in Q3. Specialized AI infrastructure providers like CoreWeave have exploded from niche GPU providers into near-top-10 global cloud vendors, generating over $1 billion in quarterly revenue from AI workloads alone.

Traditional Hosting: GoDaddy, Hostinger, and the Fight for SMBs

While hyperscalers capture enterprise workloads and AI projects, traditional hosting providers continue serving small and medium-sized businesses that need simpler solutions. This market segment remains enormous, even if it attracts less attention than cloud infrastructure announcements.

GoDaddy leads the traditional hosting market with approximately 9.29% overall share, though measurement methodologies vary. The company powers over 52 million websites and manages more than 81 million domains. In 2024, GoDaddy generated $4.57 billion in revenue, up 7.5% from 2023. The company’s dominance is even more pronounced in specific segments: GoDaddy holds 42% of U.S. shared hosting market share and approximately 63% of VPS hosting sites globally.

Hostinger has emerged as a major challenger, especially in the managed WordPress space. The company now holds the largest market share among managed WordPress hosts, appealing to price-conscious users who want more hand-holding than basic shared hosting provides. Major WordPress hosts also include OVHcloud at 3.2%, GoDaddy Group at 2.8%, Hostinger at 2.6%, and SiteGround at 2.1%.

The competitive dynamics differ between market segments. Shared hosting remains the entry point for most websites, with that segment projected to reach $70.6 billion by 2026. VPS hosting captures about 25.38% of the overall market, with the segment forecast to reach approximately $6.4 billion by 2026. Dedicated hosting targets larger businesses with critical needs, representing 17.98% of market share and projected to hit $29.6 billion by 2026, up from $16.95 billion in 2023.

DigitalOcean has carved out a strong position among developer-focused customers, powering 44% of VPS-hosted websites among the top 1 million sites. The company maintains a 23% share among VPS providers in the United States, competing effectively against larger players by focusing on simplicity and developer experience.

Industry Consolidation: Private Equity Reshapes the Landscape

The web hosting industry has experienced significant consolidation over the past decade, with private equity firms driving much of the activity. Understanding who owns what helps explain pricing trends, support quality, and strategic direction across the market.

Newfold Digital represents the largest consolidation play. Formed in 2021 when Clearlake Capital acquired Endurance International Group for approximately $3 billion and merged it with Web.com, Newfold now operates over 80 hosting brands. The portfolio includes Bluehost, HostGator, Domain.com, Network Solutions, Register.com, MarkMonitor, and Crazy Domains, collectively serving approximately 6.7 million customers globally.

Recent restructuring has organized Newfold into two divisions. The Network Solutions Group, led by Christina Clohecy, encompasses domain-focused brands. The Bluehost Group, headed by Sachin Puri, oversees hosting properties. The company has been actively consolidating brands, merging smaller properties like HostMonster, JustHost, iPage, and FatCow into Bluehost to simplify operations.

Other private equity platforms continue aggressive acquisition strategies. World Host Group acquired both FastComet and A2 Hosting, adding developer-focused and performance-oriented brands to its portfolio. European consolidators like group.one and team.blue pursue similar strategies, unifying platforms while preserving local brand recognition.

The deals keep coming because hosting businesses generate predictable cash flows. CVC’s acquisition of Namecheap and Permira’s take-private of Squarespace underscore institutional confidence in web-presence subscription revenue. These transactions typically aim to extract operational efficiencies, cross-sell additional services, and gradually raise prices once competitors have been absorbed.

For consumers, consolidation creates both risks and opportunities. Merged companies can achieve economies of scale that improve infrastructure quality. But reduced competition often leads to higher prices and sometimes declining support quality as cost-cutting takes priority over customer experience.

Regional Markets: Where Growth Is Happening Fastest

North America currently dominates the global hosting market, but the growth story increasingly belongs to Asia-Pacific. Understanding regional dynamics helps explain where hosting companies are investing and which markets offer the most opportunity.

The Asia-Pacific region is growing at 17-18% annually, outpacing all other geographies. Government initiatives drive much of this expansion. India’s “Digital India” campaign and China’s “Internet Plus” strategy encourage online platform adoption, converting hundreds of millions of mobile-only users into consumers of hosted services. The expansion of e-commerce and SME growth in China, India, and Japan creates demand for cost-effective hosting solutions that serve local business needs.

China specifically is forecast to grow at a 15.8% CAGR, potentially reaching $30.1 billion by 2030. Large-scale data center projects across the region support this growth, with major investments in infrastructure that will serve domestic and regional customers. Internet penetration and smartphone adoption continue expanding, creating ongoing demand for web hosting services.

Europe maintains substantial market share but grows more slowly than Asia-Pacific. GDPR and data sovereignty requirements create distinct opportunities for European-based providers who can guarantee compliant data residency. Regulatory frameworks that might seem burdensome actually create barriers to entry that benefit established local players.

For website owners targeting specific regions, hosting location matters for performance. A site serving German audiences benefits from nearby servers, just as sites targeting Indian users perform better with local infrastructure. The geographic distribution of data centers reflects these realities, with major providers expanding their presence across regions where demand is growing fastest.

Technology Trends: Edge Computing and CDN Growth

The traditional model of hosting concentrated in centralized data centers is evolving. Edge computing pushes processing closer to end users, while content delivery networks distribute assets across global points of presence. These technologies are becoming integral to modern hosting strategies.

The content delivery network market is projected to grow from $27.25 billion in 2025 to $42.89 billion by 2030 at a 9.5% CAGR. More aggressive estimates place 2025 valuations at $32.70 billion with growth to $144.91 billion by 2034. North America leads with approximately $9.1 billion in CDN spending, capturing around 32.5% of the global total.

Akamai holds approximately 20% global CDN share, while Cloudflare maintains 15% and Fastly claims 5%. Collectively, the top five providers manage over 60% of global CDN traffic through more than 1,200 distributed edge points of presence. Cloudflare has been particularly aggressive, expanding its network to 310+ PoPs and building developer-focused tools that make edge computing accessible to smaller organizations.

The architectural shift toward edge computing is redefining what CDNs do. According to Gartner’s 2025 Edge Trends Report, over 60% of enterprise data is now processed at the edge rather than in centralized data centers. This enables real-time application execution, ultra-low-latency delivery, and on-the-fly AI processing that traditional hosting architectures can’t match.

Survey data suggests 89% of hosting professionals now use edge computing as part of their infrastructure, with 73.7% describing it as a key component of their cloud strategy. The edge server market is forecast to reach over $8.5 billion by 2025, representing major investment in distributed infrastructure.

Cloudflare’s zero-trust security stack, enforced at the edge, has become a $300 million annual business growing faster than its core CDN offerings. This illustrates how edge networks are evolving beyond simple content caching into full-featured security and application platforms. Cloud hosting providers increasingly integrate with edge networks to deliver better performance for globally distributed audiences.

Sustainability: Green Hosting Becomes Business Imperative

Data centers consume between 1% and 1.5% of global electricity, a figure that could double by 2030 if current growth continues. A single large data center can use as much electricity as tens of thousands of homes, and digital infrastructure now accounts for more than 3% of global carbon emissions. These statistics have transformed sustainability from a marketing differentiator into a business imperative.

Greenpeace predicts the tech sector’s electricity use could reach 20% of the global total by 2025, up from 7%. This trajectory has prompted regulatory action and customer pressure that hosting companies can’t ignore. Europe’s Climate Neutral Data Centre Pact exemplifies the regulatory push toward enhanced efficiency and renewable energy use.

Major cloud providers have responded with ambitious commitments. Amazon Web Services has committed to 100% renewable energy usage by 2025. Google set an ambition in 2021 to reach net-zero emissions across all operations by 2030, aiming to run on 24/7 carbon-free energy on every grid where they operate. These commitments reshape expectations for the entire industry.

Traditional hosting providers are following suit, though implementation varies. IONOS runs its US data center entirely on wind power and uses 100% renewable electricity in Europe, with carbon offsets to maintain carbon neutrality. GreenGeeks partners with the Bonneville Environmental Foundation to offset three times the energy consumed through wind energy credits. A2 Hosting has been carbon-neutral since 2007 through Carbonfund.org partnerships.

The technology enabling these commitments continues advancing. AI integrated with data center infrastructure management can greatly enhance energy optimization, providing real-time insights and automated adjustments. Modern cooling systems reduce the power usage effectiveness (PUE) that measures how efficiently data centers convert electricity into useful computing. Containerized hosting and serverless architectures inherently improve resource utilization, reducing waste from idle servers.

Sustainability is increasingly becoming a purchasing criterion. Boards, investors, and regulators expect companies to measure, manage, and report on environmental performance through ESG reports and certifications like B Corp, ISO 14001, or LEED. Hosting providers that can’t demonstrate sustainable practices risk losing customers and facing regulatory complications.

The Foundation: 1.34 Billion Websites and Counting

Every hosting statistic ultimately connects to the websites and applications these services support. Understanding the scale of the web provides context for why the hosting market continues growing despite apparent maturity.

The total number of websites worldwide stands at approximately 1.34 billion. However, only about 201 million of these show signs of regular maintenance and content updates, just 15% of the total. Active website growth runs at approximately 5% year-over-year, which still represents millions of new sites requiring hosting each year.

Domain registrations tell a similar story. The first quarter of 2025 closed with 368.4 million domain name registrations across all top-level domains. By Q3 2025, that figure reached 378.5 million, an increase of 10.1 million domains in just two quarters. The .com domain name base alone totals 157.2 million registrations, with country-code TLDs contributing another 142.9 million.

New generic TLDs have shown remarkable growth, reaching 37.8 million registrations by Q1 2025 and increasing 13.5% year-over-year. Projections suggest new gTLD registrations will surpass 50 million by 2026, reflecting growing acceptance of alternatives to traditional extensions.

Internet usage itself continues expanding. The connected population grew from under 400 million users in 2000 to over 6 billion in 2025. Each new user represents potential demand for web services that require hosting infrastructure. In emerging markets especially, smartphone adoption is creating first-time internet users who will eventually launch businesses, blogs, and applications that need somewhere to live.

This foundation explains why the hosting industry remains attractive despite competition and consolidation. The underlying market keeps growing because the internet itself keeps growing. Every new website, application, API, and connected device represents demand that hosting providers can serve.

Segment Analysis: Shared, VPS, Dedicated, and Cloud

The hosting market divides into distinct segments serving different customer needs. Understanding these categories helps explain industry dynamics and where growth is concentrated.

Shared hosting remains the entry point for most websites. Multiple customers share server resources, making costs low but performance variable. The segment is projected to reach $70.6 billion by 2026, driven primarily by small businesses and individual site owners who need basic functionality without technical complexity. Margins tend to be thin, pushing providers toward upselling customers to higher tiers.

Virtual private server hosting captures users who’ve outgrown shared environments. VPS hosting allocates dedicated resources within virtualized environments, offering better performance and control without the cost of physical dedicated servers. The segment represents approximately 25.38% of the market in 2025, with the VPS market projected to reach $6.4 billion by 2026 and potentially $10.8 billion by 2035.

Dedicated hosting serves larger businesses with demanding requirements. Physical servers dedicated to single customers provide maximum performance and security. Over 41 million websites currently rely on dedicated servers. The segment is growing rapidly, projected to hit $29.6 billion by 2026 at an 18.9% CAGR. OVH leads the dedicated hosting market share in the United States at 13%.

Cloud hosting represents the fastest-growing segment, blending characteristics of VPS and dedicated solutions with hyperscale infrastructure. Cloud hosting is projected to advance at a 17.7% CAGR through 2030. The colocation hosting segment, where businesses place their own hardware in shared facilities, shows even faster growth at 24.3% CAGR.

Hybrid deployments, combining on-premises infrastructure with cloud resources, are witnessing the highest growth rate at 22.8% CAGR. This reflects enterprise preferences for flexibility: keeping sensitive workloads on-premises while leveraging cloud for variable demand and specialized capabilities.

What This Means for Choosing Hosting in 2026

Market analysis ultimately matters because it informs decisions. Understanding industry dynamics helps website owners, developers, and businesses make smarter choices about where to host their applications.

The hyperscaler dominance means AWS, Azure, and Google Cloud offer unmatched scale, global infrastructure, and cutting-edge capabilities. For applications requiring AI workloads, massive scalability, or enterprise integration, these platforms are often the right choice. But their complexity and cost structures can overwhelm smaller projects that don’t need enterprise-grade capabilities.

Traditional hosting providers remain relevant for simpler use cases. A small business website doesn’t need Kubernetes orchestration or machine learning inference. Providers like Hostinger, SiteGround, and others reviewed in our US hosting comparison deliver excellent value for straightforward requirements. The shared hosting segment will reach $70 billion for a reason: most websites don’t need more.

Industry consolidation suggests paying attention to who owns what. Brands that appear independent often share infrastructure and corporate ownership. This isn’t necessarily bad, but it means support experiences and pricing decisions may correlate across seemingly separate companies. Independent providers like DigitalOcean, Linode (now Akamai), and Vultr offer alternatives for users who prefer less concentrated ownership.

Geographic considerations matter for performance. Users in Asia-Pacific benefit from regionally-focused providers or global companies with strong local presence. Edge computing and CDN integration can bridge geographic gaps, but nothing fully replaces proximity for latency-sensitive applications.

Sustainability is becoming non-negotiable for many organizations. If environmental impact influences your purchasing decisions, verify provider claims rather than trusting marketing. Look for third-party certifications, published PUE figures, and specific renewable energy commitments rather than vague sustainability promises.

Frequently Asked Questions

How big is the global web hosting market in 2026?

Market size estimates range from $125 billion to $195 billion for 2025, depending on what’s included in the definition of web hosting. Fortune Business Insights projects the market reaching $149.30 billion in 2025 and $527.07 billion by 2032 at a 19.7% CAGR. More conservative estimates from Mordor Intelligence place 2025 at $194.20 billion, growing to $362.20 billion by 2030 at a 13.27% CAGR. The variation reflects different approaches to counting cloud infrastructure, managed services, and adjacent categories.

Which company has the largest web hosting market share?

AWS leads overall cloud and hosting infrastructure with 29% market share as of Q3 2025, followed by Microsoft Azure at 20% and Google Cloud at 13%. In traditional hosting specifically, GoDaddy holds 9.29% market share, powers 52 million websites, and dominates U.S. shared hosting with 42% share. The answer depends on how narrowly you define web hosting versus broader cloud infrastructure.

Which region is growing fastest for web hosting?

Asia-Pacific leads regional growth at 17-18% CAGR, driven by government digitalization initiatives in India and China, expanding SME sectors, and increasing internet penetration. China specifically is forecast to grow at 15.8% CAGR to reach $30.1 billion by 2030. North America currently holds the largest market share at 41.25% but grows more slowly due to market maturity.

How much electricity do data centers consume?

Data centers consume between 1% and 1.5% of global electricity, with projections suggesting this could double by 2030. Digital infrastructure now accounts for more than 3% of global carbon emissions. Major cloud providers have committed to 100% renewable energy, with AWS targeting 2025 and Google aiming for net-zero operations by 2030. These environmental concerns are driving heavy investment in efficient cooling systems, renewable energy, and carbon offset programs.

Looking Ahead: Industry Projections Through 2030

Projecting the hosting industry five years forward requires acknowledging significant uncertainty. AI workloads barely registered in market reports two years ago; now they’re driving 200% year-over-year growth in GPU-as-a-Service. Similar disruptions could emerge from quantum computing, new application architectures, or regulatory changes that reshape data sovereignty requirements.

What seems reasonably certain is continued growth. Every research firm projects the hosting market expanding substantially, whether the 2030 figure lands at $300 billion, $400 billion, or higher. The foundation of 6 billion internet users and 1.3 billion websites keeps expanding, and each increment creates hosting demand.

Cloud infrastructure will likely exceed $500 billion in annual spending before the decade ends. The hyperscalers will capture most of this growth, but specialized providers serving AI workloads, compliance-constrained industries, and performance-sensitive applications will carve out defensible positions. The pie grows large enough for multiple winners.

Consolidation will continue because private equity models work in hosting. Predictable subscription revenue, sticky customer relationships, and operational efficiency from shared infrastructure create attractive investment profiles. Expect more brand mergers, infrastructure unification, and cross-selling across combined portfolios.

Edge computing will evolve from specialized technology into standard architecture. The distribution of compute resources away from centralized data centers aligns with latency requirements for AI inference, real-time applications, and IoT devices. CDN providers and cloud platforms alike are investing heavily in edge capabilities.

Sustainability will transition from differentiator to table stakes. Regulatory requirements, customer expectations, and genuine cost savings from efficient operations will push the entire industry toward greener practices. Providers unable or unwilling to demonstrate environmental responsibility will face competitive disadvantages.

The hosting industry in 2030 will look different from today, just as today looks different from 2020. The constant is growth. The variable is which companies capture it, which technologies enable it, and which regions lead it. For anyone building on the web, understanding these dynamics helps navigate decisions that will shape online presence for years to come.